Turbo Takeaways

- Credit utilization compares your revolving balances to your available credit limits, helping lenders assess how well you manage debt.

- Your credit utilization ratio is a key factor used to calculate your credit score.

- Paying down balances, timing payments, and extending available credit can all improve your utilization rate over time.

What Is a Credit Utilization Ratio?

Also known as a credit utilization rate, a credit utilization ratio is the percentage of available revolving credit you're currently using. Lenders and credit reporting bureaus use this ratio to evaluate your ability to manage and pay off debt.

Credit utilization calculations focus on revolving accounts, which for many people means credit cards. Other revolving credit, such as personal lines of credit or a home equity line of credit (HELOC), can also factor in because they have a limit and a running balance.

Did You Know?

Your credit utilization can fluctuate depending on when your balance is reported and when you make payments within the billing cycle. Paying earlier can lower the balance reported to credit bureaus, helping build a stronger credit profile.

Credit utilization ratios are a major factor in many credit-scoring models, and often change month to month. Keeping utilization lower generally supports healthier credit signals, especially when paired with on-time payments.

How To Calculate a Credit Utilization Ratio

A credit utilization ratio uses two totals across your revolving accounts: the balances you currently owe and your total available credit (credit limits).

The example table below breaks those numbers out by account so you can see how the totals are built before calculating your overall utilization percentage.

| Revolving Account | Debt Balance | Available Credit |

|---|---|---|

| Credit Card A | $2,000 | $12,000 |

| Credit Card B | $1,500 | $10,000 |

| HELOC | $4,000 | $50,000 |

| Total | $7,500 | $72,000 |

Start by adding up the balances on each revolving account, then add up the available credit (credit limits) for those accounts. Once you have those two totals, divide your total debt balance by your total available credit.

In this example, the total debt balances add up to $7,500, and the total available credit is $72,000. Dividing those totals gives $7,500 ÷ $72,000 = 0.1042, or 10.42% (typically rounded to 10%).

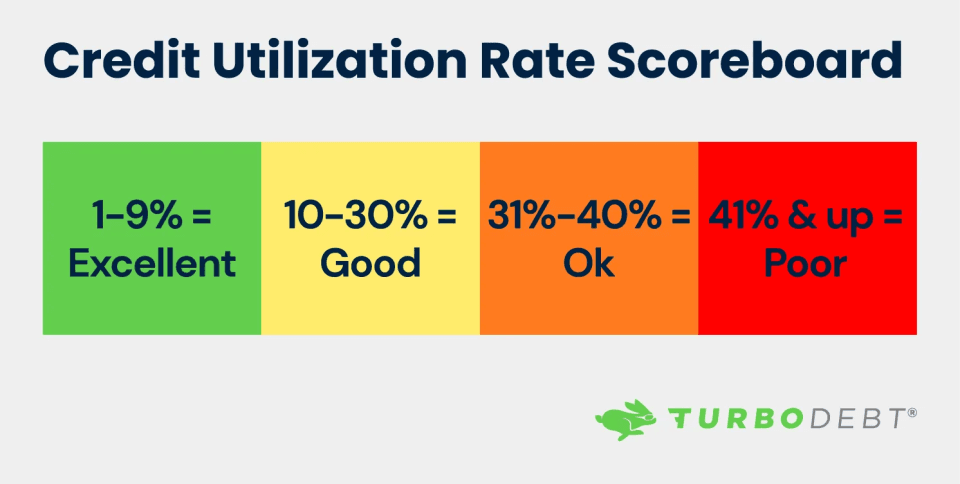

What Is a Good Credit Utilization Rate?

When it comes to credit utilization, the lower your ratio, the better. Experts suggest that a credit utilization rate of 30% or less is best, while a score in the single digits is ideal to secure excellent credit.

Lower ratios can also prove that you’re able to pay off debt and are less of a risk for lenders. Using credit within your limits and quickly and consistently paying off balances are some key strategies to maintaining an effective credit utilization ratio.

Recent statistics show an average credit utilization rate hovering just below 30% across the country. This proves that many American consumers maintain a reasonable credit utilization ratio that contributes to an effective credit score.

How Does a Credit Utilization Ratio Affect Your Credit Score?

Your credit utilization ratio is one of the biggest contributors to your overall credit score, second only to payment history with some reporting bureaus. Since your utilization weighs so heavily on your credit score, a high ratio could drag your score down, making it a challenge to open new lines of credit or secure a loan at a decent interest rate.

However, credit reporting bureaus calculate utilization rates based on your most recent balance history versus your available credit. Even if you’ve struggled with large balances in the past, your current balance versus your credit limits is what’s used to determine your score. That’s why it’s important to be proactive in paying off debt and keeping balances low.

As soon as you start reducing your account balances, your credit utilization ratio drops, making it one of the quickest ways to improve your credit score.

7 Strategies to Improve Your Credit Utilization Ratio

Credit utilization can shift faster than most parts of your credit score, which is why small changes in how you pay and manage limits can make a meaningful difference. The strategies below focus on practical moves that keep utilization lower without creating new debt.

- Pay Off Balances

The faster you pay off revolving balances, the quicker your utilization rate can improve. Because card issuers may report balances during the billing cycle, lower balances can show up on your credit report sooner. - Ask for a Higher Limit

Raising your credit limit on one or more accounts may also improve your utilization rate by increasing your available credit. With a higher credit limit versus your balances, your ratio typically drops. - Spend Below Your Old Limit

A higher credit limit can be tempting, but keeping purchases near your previous limit helps lower utilization while avoiding new debt. This approach works best when spending habits stay about the same. - Open a New Credit Card

A new card can increase your total available credit and reduce utilization, especially if you keep balances low across accounts. Some cards may seem tempting with perks like cash back or travel points, but only apply if terms are favorable and you can manage another account. - Make Mid-Cycle Payments

Your utilization rate can fluctuate depending on when it’s reported during the billing cycle. Making an extra payment mid-cycle can lower the balance that gets reported and may help improve your utilization faster. A pay-as-you-go approach can also make you more aware of your spending and help you budget. - Avoid Closing Older Accounts

Closing a card can shrink your available credit and raise utilization overnight, even if spending doesn’t change. If an account has no annual fee and you can manage it responsibly, keeping it open often helps keep utilization lower. - Explore Debt Relief Options

If debt feels unmanageable, a debt relief program may help you structure payments and reduce your balances. Results vary by provider and financial situation, so compare costs, timelines, and eligibility carefully before enrolling.

Reduce Your Financial Burdens With TurboDebt®

If you’re struggling with credit card debt or other large balances, you may face a higher credit utilization ratio. The best way to lower your rate is to reduce and pay off debt as fast as possible.

At TurboDebt®, it’s our mission to help consumers overcome financial struggles by connecting clients with the best options for debt relief. We’ve already enrolled millions of dollars in debt into our program, helping thousands of American consumers reduce their total debt and pay off balances faster.

Over 20,000 positive reviews across Trustpilot and Google prove we’re a trusted partner for eliminating unsecured debts.

All it takes is a few minutes to start a free consultation with one of our expert team members. Contact TurboDebt today to begin your debt relief journey!